| It is the most important financial decision anyone will ever make. Yet people are incredibly ignorant of the most basic rules. They have no clue how the mortgage industry really works.

A mortgage company gives out money in exchange for a promise to pay back installments of money. The mortgage company secures the property by receiving a contract for certain penalties if the money does not get paid back as promised; this could include seizing the property. This is less risky for a mortgage company than unsecured loans (such as credit cards) because there is collateral (the house) for it to seize. Therefore, it can afford to demand less money be paid back–a lower interest rate. Mortgage loans usually have the homeowner making monthly payments for 10,15 or 30 years. This monthly payment includes a portion of the total amount borrowed (principal) and an amount determined by the interest rate on that principal amount. Once the full amount borrowed (principal) gets paid back the mortgage is fulfilled. Who is involved? The lender (aka mortgagee) owns the loan and agrees the terms. They have an investor who helps provide the funds that get handed out. They use an underwriter to determine if the arrangement will earn them a profit, based on the property and the credit of the mortgager. Usually the lender authorizes a servicer to deal with everything about the mortgage. The servicer collects payments, secures the property, and negotiates modifications. The servicer could get additional parties involved, such as property inspectors. The trustee on the securing document conveys the title when the loan is paid off or holds the power of sale in the case of a foreclosure. Documents involved The process begins with the application, which upon approval offers a tentative agreement–this origination agreement can vary in form by state. Most places require a disclosure of terms of the agreement so the mortgager knows what to expect. But the terms can still change. The promissory note sets the final terms. In order to better secure the loan, the lender will establish a lien on the property with a security instrument, known as a mortgage or deed of trust. |

|

The security instrument pretty much sets the rules for what the lender can do if the money doesn’t get paid back as promised (aka defaults).

Make sure to check the grace period (length of time you can pay late without getting charged a late fee) which often is 15 days, and how large the late fee is. Sometimes it could be ridiculously large, and sometimes it could even be zero. The late fee is usually proportionate to the principal balance still owed, so it will be a small amount near the end of the loan.

Also read the contract’s stipulations for reporting to the credit reporting bureaus. Check your servicer for their policy on credit reporting. Read each document very carefully with a legal counselor present! The buyer should also research state and federal lending laws.

What type of loan to get?

Adjustable– Do not get an adjustable rate mortgage unless you are sure you will refinance, sell, or modify soon. This kind of loan starts with a teaser interest rate that will probably rise toward the ceiling (highest allowed) rate. The note determines how quickly the interest rate can change, usually by 2 or so percent each month. Many people get ARM loans and end up defaulting because the cost rises very high. The amortization schedule determines at the beginning of the loan how much principal due will get paid each payment. But the interest rate could rise to any amount within the ceiling. The interest rate is determined a month in advance because mortgages are paid in arrears– the interest you pay is actually for the portion of principal due the previous month.

Fixed-rate traditional mortgages (aka conventional mortgages) amortize at the beginning of the loan how much principal and how much interest will get paid each month until the very end. Your payment will not change unless escrow gets involved or unless the loan gets modified. Loans could mix a traditional and ARM loan, with some years fixed and some years changeable interest rates- though this never really makes sense to do.

Balloon loans amortize very briefly so that all the principal you pay over the months doesn’t add up to amount borrowed. As a result there is still a large amount left over due at the end, and must be paid all at once. Don’t get this loan unless you are sure you can refinance at that point or receive a large amount of money before then.

Daily Simple Interest usually applies to car loans rather than mortgages. This loan is good if you expect to be able to make large payments at random times. Extra money paid will pay down the principal quicker and decrease the amount of interest you will have to pay. With other loans if you pay more than what is due for principal and interest, the servicer may apply that toward your next month payment, or hold it in suspense, or use it to pay down more principal. With DSI loans the amount of interest due changes every day. Each day, the principal balance still due at the end of the proceeding day is multiplied by the interest rate divided by 365. This type of loan will save you interest payments and get you paid off quicker if you can pay early or pay extra, but if you fall behind it will cost you more– because the day you go late there is more principal left to be paid back than what was expected and the next day’s payment will therefore be higher than expected. Even if you are one day late and within your grace period you will have more to pay. Principal doesn’t get paid until all the interest due gets paid, so people often get so behind that the interest due builds up and principal doesn’t even get paid anymore. That is really bad news. Often people will have a chunk of money to pay back at the end of this loan because of those months when they paid a couple days after the 1st.

Interest Only mortgages are pretty much the same as renting the property. The homeowner only pays for the monthly interest due, and all that principal borrowed sits there still due. At some point the homeowner will start paying for principal as well, and then the principal will get paid off month by month as another type of loan until the mortgage is finished. This type of mortgage should only be used if you are confident you will refinance, modify, significantly increase your income, or sell soon. It makes no sense to pay money each month if what you owe for buying the property never goes down. Some loans make it an option to pay principal as well as interest.

Option ARM loans give the mortgager the option to either: pay everything due each month, pay interest only, or pay a small minimum amount. The minimum amount doesn’t pay all the interest due that month (negative amortized) so it builds up next month and quickly becomes a large amount due later on. This type of loan is never a good idea and never should have been created in the first place. If the homeowner receives a large income every couple months they should either get a DSI loan or save a portion of those funds for each monthly payment. It is an unnecessary risk to sacrifice home equity.

Piggy-back mortgages are also never a good idea. This is a combination of two loans to avoid a down payment over 20% of the borrowed amount. But paying for two loans instead of one doesn’t do any good.

Graduated Payment mortgages are amortized past their maturity date. In order to avoid a balloon payment at the end, the payment amount increases month by month. This is intended for younger people who expect larger paychecks over the years. But it is hardly used any more. Young people don’t have the credit for it anyway.

Government loans are just too complicated these days… so I won’t begin trying to explain it all. Government loans often have extra protections and lower rates that make them preferred. But good luck getting good service!

Reverse mortgage– Use only if you are desperate. A person who has been paying their mortgage for many years has a good fraction of their principal paid off. With this mortgage, the amount of this principal owed increases each month rather than decreases in order to make past-due monthly payments.

How does my payment apply?

Each loan is set up differently and each servicer has a different hierarchy for how payments apply. Principal and interest could end up not getting paid if the payment only covers what is due for fees first. Your top priority is to pay off principal because that is what interest gets charged from, and once it’s paid off the mortgage is finished (unless fees and escrow are left over due). DSI loans pay interest before principal. Again, check with your documents and servicer’s policy to see how it actually applies because everyone is different.

Depending on your loan type any extra money paid (after interest accrued and fees) should pay down the principal. Your note will list under fees if there is a penalty for paying a certain amount extra early (aka prepayment penalty). In order to pay off the loan you will need to pay (at least) all principal left, interest accrued, escrow advanced, DSI interest short, fees due, and lien release fee. The servicer totals this up in the payoff quote.

What about divorces, transfer of ownerships, death of owner, etc?

Divorce only effects the mortgage if both persons are listed as mortgager or co-mortgager (not just an authorized party). Otherwise the spouse never had any liability with the mortgage in the first place. Some states require the spouse to be authorized as a third party in order to handle the account if they aren’t on the mortgage. Other states allow the servicer to handle the mortgage through the spouse without the mortgager’s authorization. Even if you are separated from the spouse in these states, they can still possibly handle the account until the divorce is completed. Check with your servicer for their policy as each servicer varies. It is entirely up to the court to decide who gets ownership of the house and mortgage, and the servicer may require court papers to take the ex-spouse off the mortgage. It could work out so that a transfer of ownership takes place through a quitclaim deed. Transferring the mortgage requires a refinance.

Transfer of ownership– Unless the mortgage is finished (aka discharged) or refinanced at the time of the sale, the lender will probably want the the house sale to be “subject to lien”, which means the original owner retains the mortgage. The note should clearly state such terms in the case of a property sale. Most people pay off the mortgage with the amount earned by the sale (which may cause a penalty, see fees listed your note). Consult a real estate attorney to make sure you don’t commit an unauthorized transfer of ownership that could amount to a strawman buyer or other such fraud.

Death of Owner– The co-owner/owner retains interest in the property and holds the mortgage if the owner/co-owner dies; authorized third parties do not. Family members or friends need to provide an Executor of Estate to become authorized to handle the account unless they were already an authorized third party (and that authorization didn’t expire). Some states allow the servicer to handle the account through the spouse. This does not give the spouse, executor of estate, or third party ownership or liability unless they get a refinance or court order. Check your servicer’s policies regarding this as each servicer varies.

What is Escrow

A mortgagor will pay a certain amount extra each month that goes into a separate escrow account, a lump of funds from which the servicer pays the mortgagor’s house taxes or insurance. The servicer will often pay a mortgager’s delinquent taxes or insurance, because it is in the servicer’s interest to secure the property. The servicer will then open an escrow account with an advanced balance that needs to get paid back by the mortgagor. They should not charge interest on an advanced escrow balance.

The servicer almost certainly requires the mortgagor to have insurance, as stated in the note, and keeps careful track of the mortgagor’s insurance and tax status. It is up to the mortgagor to provide proof of insurance. The servicer should attempt to notify the mortgagor before they open an escrow account, but the note and law probably allows them open an escrow account without the mortgagor’s authorization.

Escrow is good because it saves the mortgagor the burden of paying a huge tax bill all at once. Although, some people pay it with a lump income like a tax return; it depends on your circumstances. Check with your servicer if they pay interest on the funds sitting in your escrow account. It also saves the mortgagor the stress of paying those bills. It is in the servicer’s interest to pay escrow because it makes the property more secure; it won’t go to tax lien or be without insurance.

It is good to keep track of the funds paid into the escrow account and disbursements made to taxes and insurance, but it often becomes quite complicated. There is no reason the servicer should pay a fee for this service.

The servicer may accidentally charge too little each month, and the account is drained prematurely. They will then simply raise the amount due each month with a little extra for that past amount. Very often the taxes and insurance payments will be different from what the mortgager expects, so the monthly payment turns out to be off. They will either refund or credit the mortgagor the left-over amount, or raise the monthly amount if it was short. But check with your servicer as each policy is different.

How do I get it? Get rid of it?

The note and law probably allows the servicer to keep the mortgagor on escrow; check your origination documents and the laws. Each servicer’s policy is different regarding if they will drop an escrow account. The mortgagor may have the escrow account for the rest of the loan. Some subprime loans require at signing for the mortgagor to be on mortgage insurance as extra protection for the lender.

The servicer should be thrilled to get a request for an escrow account, as it provides them better security. Simply request it if that works best for your circumstances.

Federal law indicates: “Within 45 days of establishing the account, the servicer must give you a statement that clearly itemizes the estimated taxes, insurance premiums and other anticipated amounts to be paid over the next 12 months, and the expected dates and totals of those payments”, and an annual statement. The servicer can apply forced place insurance if the customer fails to keep current insurance on the property. If force placed insurance was applied in error, provide proof and they should refund you.

What is a Modification? Refinance?

Foreclosure is very costly for a lender. One report says the typical cost to mortgage companies is $60,000. A modification is an agreement by both the mortgagor and the lender to change the mortgage contract. Anything can be changed. Lenders could extend the length of the loan with a more spread out payment in order to lower the monthly amount, eliminate principal owed, move past-due payments to the end of the loan, or lower the interest rate (per about.com).

It is foolish for mortgage companies to grant a large amount of modifications with lower interest rates, because lower interest rates create a false impression that these loans are less risky than they really are. The lender is unable to lend out funds unless they receive more compensation with higher interest from loans that are riskier, and loans that default are most risky. For this reason the number of modifications granted should be kept very small. In order to help lenders grant more modifications the government created programs like HAMP that provide extra incentive.

A refinance is where another lender pays the amount of money required to remit the mortgage in full, and then sets up a fresh new loan with the mortgagor. It is hard to imagine this ever saving the mortgagor money in the long run, but they may offer a mortgage with a lower interest rate and longer term. No lender is likely to offer a refinance for a severely defaulted loan because the mortgagor’s credit score needs to be good.

Do not pay anything up-front for a modification. Many companies claim in commercials that they can get you a modification, but in my opinion it is unnecessary for another company to get involved at all. Only seek this kind of help if you are at wits end, and only pay anything after the modification is completed; even if they give you a guarantee. There are great non-profit organizations that help people to get modifications, like HOPE, NACA, and HUD if you feel like paying nothing at all for that service. The homeowner should be able to navigate through the modification process on their own- if it is feasible at all! The servicer itself should not charge anything for a modification, but check with your servicer on its policies.

How to get a modification?

Forclosure is what the servicer wants to avoid, some say, and you need to “convince the loan owner that a modification is in HIS best interest.” I can’t comment on specific policies of servicing companies, but many people pay late to give this impression.

This is a gamble. Paying late could hurt your credit, add up late charges, and start down a slippery slope that racks up a huge bill. If the modification ends up being unsuccessful the mortgagor is then stuck with an enormous bill and poor credit.

Ask yourself this objectively: How will they be convinced that a modification is necessary- and yet convinced that the mortgagor will not default even if it is modified? How many people get spectacular modifications and then fail to pay even that, and the property goes to foreclosure? It makes sense for the servicer to be keen with loans that can’t be saved even by a modification, to determine if the mortgagor is in a position to afford the new modified amount. If not, why shoud the servicer modify the loan? Keep this in mind and check with your servicer for how they determine eligibility, as each servicer is different.

Some people lose a sustainable income and dip into their savings to pay the bill until their savings run out, and then seek immediate help. My advice is to plan long-term if it becomes apparent that your income is not sustainable to pay the mortgage. Make it apparent to the servicer that the modification is necessary for their interest, and that you can pay a lower amount with a modified interest rate. Do the math yourself, laying out your income versus the present and modified monthly payment. And always keep trying again if you are turned down the first time.

Be prompt with providing information and making payments. Check with your servicer for their policy on timetables. Don’t be angry if you get denied for a modification, because they were never obligated to modify anything. You signed the same contract they did and they never came to you asking for a higher interest rate.

What information do I give for a modification?

Each servicer has different rules, and again I can’t comment on any specific policies. Seek a qualified agent. Just be honest with your explanation of your hardship and get clear instructions from your servicer. But the government puts certain rules on their modifications (2011 requirements):

Documentation required for HAMP: The new government programs stipulate requirements for participating servicers/lenders in these stimulus programs, though each servicer has different policies and your servicer could have additional requirements. If servicers/lenders participate, HAMP rules require the applying mortgagor to provide at least:

(a) Snapshot of monthly budget, (b) 2 recent pay stubs for each wage-earner on the note, (c) a 4506 T form filled out with signature of each borrower/coborrower, (d) federal Tax Returns, (e) and each signature on an Affidavit.

For other kinds of income: Self-employed people need a year-to-date profit and loss statement. Social security, disability, etc. need receipts of payment and documented evidence of the amount and frequency. Income from unemployment must continue for the next 9 months. For rental income, provide a Schedule E form and if it is your primary residence state an income of 75% of your gross. Alimony and child support don’t have to be stated, but require documentation if included. Part-time or rental income does not have to be included unless it is at least 20% of a person’s total income. Income from members of the household who are not listed on the mortgage (such as a spouse) are not required as part of the total gross income, but may give given.

HAMP Unemployment Program info here!

HAMP eligibility requirements include:

(a) Existing monthly payment on the mortgage must be more than 31% of the homeowner’s gross income for the month. Add up your gross income for the month (including the voluntarily given income if you want). If that is less than 31% of your monthly mortgage bill (excluding escrow and fees) you are eligable.

(b) Demonstrate imminent default by providing some kind of financial hardship.

(c) Principal owed must be less than $729,750.

(d) The mortgage must have began before January 1, 2009.

(e) The property must be the mortgagor’s primary residence (not a rental).

After HAMP passes, the homeowner gets set up on a 3-month trial plan. If the homeowner fails to pay these 3 payments on time the whole thing falls through. This trial payment could actually be larger than the existing payment if the loan wasn’t already escrowed for taxes and insurance. Pay careful attention to the promised new amount and consider that escrow increases it. After the 3 months is up (NOT ONE DAY earlier or one day later) the homeowner begins the new modified payment. The servicer may not modify the loan at all without the mortgagor’s and co-mortgagor’s consent. They could offer a modification even without anyone applying, but read the new contract carefully to see if it is in your best interest. More on HAMP….

HAMP requires escrowed taxes and insurance, so if your circumstances are hurt by taxes and insurance getting paid that way, consider that applying for HAMP could mess you up worse. Check with your servicer to see if this is their policy. Each servicer has different policies for modificatoins.

You Rights As A Morgtagor

Debt collectors– FDCPA guidelines restrict what the servicer can do to collect from a delinquent mortgagor. The servicer is considered a debt collector when a loan in delinquent and they attempt to collect on the debt. In such cases they must provide certain debt collecting disclosures and follow guidelines. Each servicer has their own policies, but federal law states they must: (a) Only call 8am-9pm unless requested. (b) Not call at place of employment, if told not to by the mortgagor/comortgager. (c) Not contact by phone, if such a request is received in writing from the mortgagoer/comortgager. (d) Not discuss the mortgage except with the mortgager/co-mortgager, a person they have authorized to the servicer (or non-obligar spouse in states that allow this), or representative lawyer (e) Not harass people (threaten violence, blacklist, use foul language, make false accusations of criminality, make false claims of legal authority, make false threats of foreclosure or other legal action, misrepresent amount owed, misrepresent their company name, etc). (f) Call repeatedly back-to-back (it’s still fuzzy how often is too often for phone calls)

State laws may have different restrictions and each servicer has its own policies within federal guidelines. Consult an attorney for specific federal and state laws about your rights, as I am not a lawyer.

Validation of debt letters must be sent within five days of the very initial contact, and the mortgagor then has a window of 30 days to dispute the amount owed or the creditor. The mortgagor can request a VOD letter to be sent so they can dispute the loan.

Misapplied funds: The servicer could misapply funds if the customer has multiple loans with them or the customer requests the funds to apply differently than the servicer’s application policy. This could indicate a delinquency status and poor credit reporting. The servicer will determine if the customer failed to communicate their intention properly, if they requested to apply the funds outside of what their policy allows, or if it was indeed the servicer’s fault. If it was the servicer’s fault they should reverse the damages and apply the funds correctly.

Fees are based on what the note/securing document allow, and state/federal law allows. The servicer must post the payment when it is received (not when sent, it could be delayed in the mail). The servicer is allowed to take certain steps to secure the property as the loan reaches a certain delinquency level. Federal guidelines indicate: “These services may include property inspections to make sure you are still living in the home and maintaining the property. If the property is not being properly maintained, the servicer may order “property preservation services,” like lawn mowing, landscaping and repairing or boarding up broken windows and doors. The costs for these services, which can add up to hundreds or thousands of dollars, are charged to your loan account. If the servicer starts to foreclose on your property, additional costs like attorneys fees, property title search fees, and other charges for mailing and posting foreclosure notices will be charged to your loan account.”

The servicer is not responsible for a bill pay error by the bank, or mail that is late/lost. The servicer may not let a customer know when they become delinquent, and the customer may mistakingly keep paying too little or too late. Perhaps the payment went up for some reason. It is the customer responsibility to keep track of how much the payment is and when it is due. The note specifies when the servicer must send a delinquency notice, and each servicer’s policy is different.

Inquiries and Disputes must be responded to, if submitted correctly. They have 20 days to acknowledge receiving the inquiry, and 60 days to make a determination.

Each servicer has a different policy about disclosing who the lender is. The lender might not want to hear from you directly but have the servicer handle everything.

Fair Housing– Federal regulations prevent any company from refusing to purchase a loan, from setting different terms or conditions, or from refusing to provide information regarding loans based on: race, color, national origin, religion, sex, familial status or handicap. The company can not “make any statement that indicates a limitation or preference” in this regard.

Transfers– The loan can be sold or transferred to a new servicer. “In most cases, your current servicer must notify you at least 15 days before the effective date of the transfer, unless you received a written transfer notice at settlement. The effective date is when the first mortgage payment is due at the new servicer’s address. The new servicer must notify you within 15 days after the effective date of the transfer.” A new lender has 30 days from attaining the loan to notify the customer.

The mortgagor gets a 60 day grace period the first month after the transfer and certain states require the late fee after that to be influenced the date of that first payment. Check an attorney, state laws, and your note to determine your policy in this regard.

Why don’t I have more rights?– Keep careful written records of all your communications and dealings with the mortgage company, and then retain an attorney if you feel you have really been wronged. Laws already bend over backwards for homeowner’s rights. Back in the day people were imprisoned and killed for failing to pay a debt. Personally, I think Americans feel way too entitled about receiving a huge amount of cash on a loan and then failing to pay it back as agreed. Read what you sign and expect the worst to happen in the future. Each state has different laws about recording phone conversations, and each servicer has different policies about it.

How does a loan go to foreclosure?

Late charges and other fees snowball as late monthly payments pile up over-due. Each servicer has different policies about which fees are accrued and when, and if some fees can get waived. As soon as the payment is late the foreclosure process could begin and the servicer can notify the mortgagor of this, although they can’t foreclose on the property right away. Your note and applicable laws determine the foreclosure process.

Typically the servicer can send a notice to accelerate at 60 days past due, depending on the state and previous delinquency history. A demand letter is also sent with a date when the payment needs to be made by to avoid foreclosure. After this, the servicer sends a notice of default that gives about 20 days for response before the notice of sale. Each state has different timelines for how long the court gives before the sale (judicial vs. nonjudicial foreclosure), and it could be a considerable length of time. The notice of sale sets the auction date. The mortgagor will likely be responsible to pay attorney fees for each step in this process. Check with your servicer for their policy as each is different.

The servicer can no longer accept less than the entire total amount once it reaches the notice to accelerate. Loss-mitigation could still reinstate from foreclosure for a workout solution: modifying the loan, negotiating a short sale, or with a deed in lieu. Each servicer has different polices about loss mitigation.

Deed in Lieu is when the mortgagor gives over the collateral property in order to be released from all obligations of the mortgage. Second mortgages complicate this process.

Bankruptcy is a declaration of a person’s inability to pay his creditors. Chapter 7 is the most common type of bankruptcy for homeowners, though Chapter 13 is considered by many a good alternative if there is more than nominal non-exempt equity on the property. A discharged bankruptcy eliminates the mortgagor’s personal liability for the mortgage but the lender still can foreclose on the property if it doesn’t get paid as promised. The mortgagor may reaffirm the debt after the bankruptcy is discharged. There are special regulations that must be followed for debt collectors in the case of a bankruptcy. Make sure to consult a bankruptcy attorney to determine how to retain your home as you declare bankruptcy. My advice is to consider bankruptcy if other debts besides the mortgage appear insurmountable.

Short Sale is a sale of a property for less than the principal owed, yet could release the mortgagor from obligation to pay the rest. A real estate agent negotiates with the lender for how much is enough for such a sale. Keep in mind that there could be tax implications for certain sales. Consult with a real estate attorney to determine if this is a good option for you, and then prepare the necessary documentation for your real estate agent to submit.

Tips: Avoiding fraud

Equity skimming happens from improper refinances. The lender refinances the mortgage while skimming a chunk of the equity into their pockets. The refinancer might claim the mortgagor only needs to pay rent while they secretly foreclose on the property. Be very careful who you refinance or get a second mortgage with and skeptical of good deals.

Property flipping involves a broker in league with a buyer, seller, and appraiser. The property is sold to a strawman buyer with an inflated value of the home from a fraud appraiser. This property is then sold for an even higher inflated amount to an honest buyer or false identity and the strawman walks away with a higher amount.

Identity theft is a buyer assuming someone else’s identity and credit to buy or sell a home.

It is very risky to take on a second lien to get out of debt from the first, or to refinance to get out of debt, so make sure to get a real estate counselor before giving away any information. A second lien might, for example, fraudulently foreclose on a property to take the equity from the first lien. If there is only a little amount left to pay on the first mortgage and the mortgagor takes out a second loan, that second company could earn a lot by fraudulently foreclosing, paying off the rest of the first loan, and seizing the property. Be wary of a becoming a strawman buyer’s victim, of identity theft, and of fraudulent refinancing. Seek a qualified lawyer for specific information on fraud threats.

Insurance/taxes– The mortgage company usually secures itself as a payee signer, which means that any insurance claim must be signed and approved by them. Seek a qualified lawyer to see if your insurance situation is shady. The mortgage company likewise should keep track of a mortgagor’s property taxes in case the mortgagor stops paying.

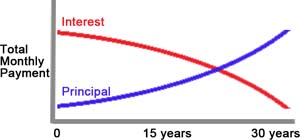

Why is my payment mostly for interest? The amortization schedule on promissory note determines for the next 30 years (or whatever) how much principal and how much interest to include in each month’s payment during that time to get it paid off by the end. Almost all the monthly payment will apply to interest at first because there is such a large amount of principal still owed. Slowly that principal decreases and the monthly interest dramatically decreases. When the interest payment is lower that means the rest goes to principal. This works out so that most of the monthly payment will apply to interest until about two-thirds the way through the loan, and then it will dramatically switch where most of the payment applies to principal. It just works out that way.

Billpay is a separate bank account that the mortgagor pays into, which the bank then releases to the servicer to pay the monthly bill. The mortgagor usually doesn’t earn interest from the time those funds are in that other billpay account (this is why the bank likes billpay), and the bank usually just puts a check in the mail, so it really doesn’t do the mortgagor any good. If the mortgagors just holds on to the money themselves and put a check in the mail when the bill is due, they at least earn a little money during that time it would be in billpay. The mortgagor could set up a seperate checking account that automatically receives the same amount each month and pays that to the servicer through automatic billing or an online service. Check with your servicer for what their charges are for online or other services to make payments.

Conclusion: The Architect’s Larger Role

Reliance on the owner to competently finance projects has ruined the construction industry. Very basic knowledge of mortgages as explained in this article is uncommon. Particularly as more architectural projects deal with restoration of existing buildings, it should fall on the architect as the owner’s advocate to secure financing. The architect transforms from engineer to planner over the years, but this is perhaps as it was always meant to be. Vitruvius inistated that architects take care to design buildings according to the financial class of the client. America’s age of McMansions and foreclosures prove this advice goes unheeded.

The pernicious nature of America’s entitlement mentality caused the Real Estate crash. Companies said they could compassionately put people in homes they really couldn’t afford, and the people did anything they could to get the home. It is extremely disturbing that the homeowner is so eager to bind himself at the mercy of creditors, but it is realistically necessary that some kind of credit be used to finance the home. The common homeowner and business needs an architect as an advocate to determine what is affordable and to get a loan that is feasible. Unfortunately, people look to the government to do this, or to force mortgage companies to be more compassionate. This can only do more damage, perhaps as much damage as the governmental subsidies for sustainable designs really never leads to greener environments. Our buildings are continually less environmentally sustainable, and at the same time less financially sustainable. The government’s role is to prevent fraud and cheating; that’s it. It is up to the owner, and the owner needs an architect.

***No part of this article should be considered legal advice and it creates no kind of counselor/client relationship to the reader. The author is not a licensed lawyer. Each mortgage involves different laws and regulations, and so the reader should consult a real estate attorney before making any kind of financial or legal decision. Information here may not be correct for a specific mortgage’s circumstances or due to changing rules, and is not necessarily correct. The author intends no disclosure of proprietary information or any company’s policies/procedures; all information is general and not specific to any person or company.***

All text and images copyrighted